Upcoming Event

Free Newsletter

Free Newsletter

For Retirement: Avoid the Target-Date Fund Trap

Target-date investment funds purport to be optimized for specific retirement years

Timothy J. Keating //June 19, 2019//

For Retirement: Avoid the Target-Date Fund Trap

Target-date investment funds purport to be optimized for specific retirement years

Timothy J. Keating //June 19, 2019//

Conventional investment wisdom states that as you near retirement, you should adjust the allocation of your investments to a supposedly safer mix of assets that favors bonds over equities. This solidly ingrained tenet has fueled the popularity of target-date investment funds, which purport to be optimized for specific retirement years.

Introduced in the early 1990s, target-date funds each own a group of other funds and adjust the proportions of assets allocated to each sub-fund as time progresses. Investors choose a fund with a date matching their anticipated retirement year. A fund with 2040 in its name, for example, is geared for people planning to retire in or near that year.

According to Morningstar, assets managed using target-date strategies totaled more than $1.7 trillion at the end of 2018, including $1.1 trillion in mutual funds and $660 billion in collective investment trusts. The mutual fund segment alone has experienced a seven-fold increase from the $158 billion invested at the end of 2008. In 2018, there was a $55 billion net inflow to target-date mutual funds.

Meanwhile, the Investment Company Institute reports that 70% of all large 401(k) retirement plans now offer target-date funds as options. Indeed, the most recent data from the Employee Benefit Research Institute and the Investment Company Institute show that target-date funds held 21% of all 401(k) plan assets as of year-end 2016, quadruple their 5% share in 2006. About half of all plan participants now elect target-date funds for some part of their portfolios.

Similarly, Vanguard reports that half of its 401(k) plan participants currently invest their entire accounts in a single target-date fund. Vanguard projects that this figure will rise to 70% by 2022. At the current trajectory, it’s only a short matter of time until target-date funds cross the 50% threshold of all 401(k) assets.

A big factor in the explosive growth of target-date funds is the fact that they are usually the default investment setting for new hires automatically enrolled in their employers’ retirement plans. This has been the case since the implementation of the Pension Protection Act during the Obama administration.

Compelling Features as Default Choice

Target-date funds are clearly superior to the previous status quo: either not saving for retirement at all or accumulating cash through inattention to investments.

Moreover, target-date funds have many compelling features. Through a single, low-cost mutual fund, an investor can own a diversified portfolio and put all investment and rebalancing decisions on autopilot. You can’t beat these funds for simplicity, and when investors combine them with a “set it and forget it” discipline, they avoid many behavioral errors such as trying to time the market.

The Downside: Savings Need to Last Longer and Grow

The deadly trap of target-date funds is that once investors reach their target retirement year, their allocation to bonds is always too high.

Consider, for example, the Vanguard Target Retirement 2040 Fund (VFORX). The fund invests in four Vanguard index funds, and at the end of May 2019, it held approximately 85% of its assets in stocks (51% domestic and 34% international) and 15% in bonds (10% domestic and 5% international).

The fund slides to a more “conservative” asset allocation over time, so that in 2040, it will consist of 49% stocks, 43% bonds, and 9% short-term Treasury inflation-protected securities, or TIPS. Five years later, the portfolio will be allocated 37% to stocks, 49% to bonds, and 14% to short-term TIPS, which are designed to provide a “real” return and protect investors from the eroding effect of inflation. As of May 31, 2019, the 30-day SEC yield of Vanguard’s TIPS fund (VIPSX) was 0.38%.

Longevity Risk

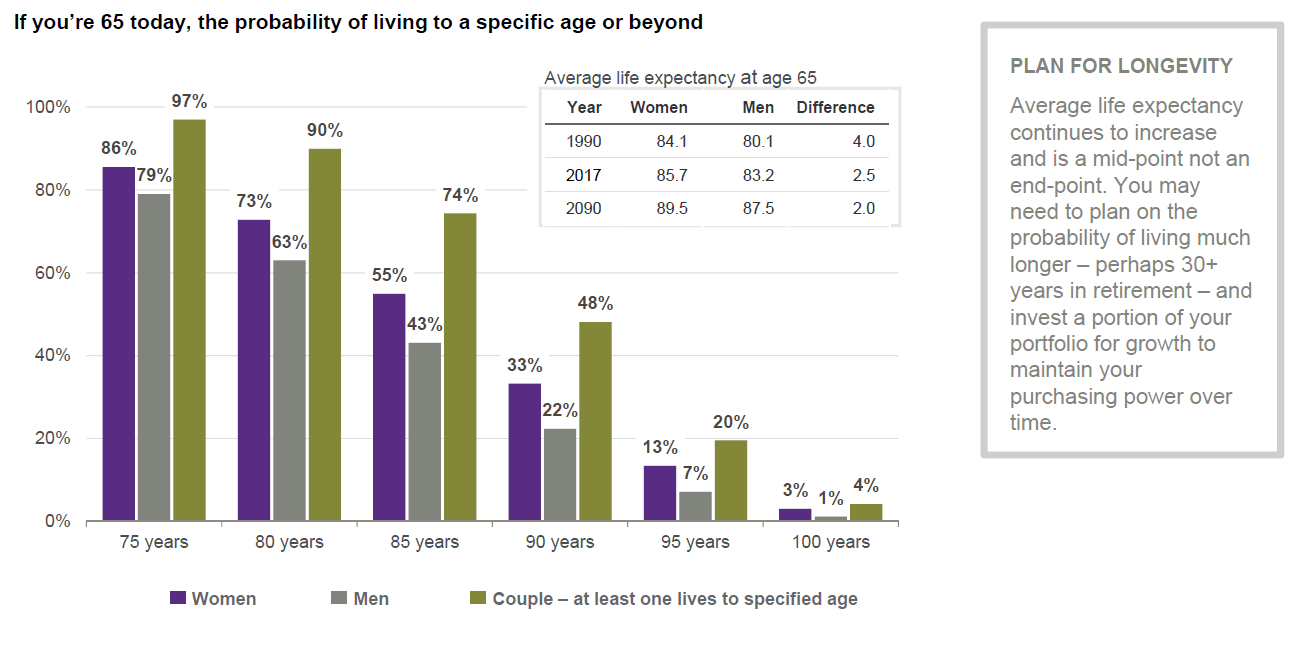

The problem with bond-heavy portfolios in retirement can be distilled to a single word: longevity. Average life expectancies continue to increase. As J.P. Morgan Asset Management notes: “You may need to plan on the probability of living much longer—perhaps 30+ years in retirement—and invest a portion of your portfolio for growth [that is, in equities] to maintain your purchasing power over time.”

Source: J.P. Morgan Guide to Retirement, 2019 Edition

While there is no guarantee that historical equity returns will continue indefinitely into the future, a century of experience suggests that the compounded return of equities will very likely exceed that of a bond-dominated portfolio over any 20- to 30-year time horizon.

A Good Nudge Gone Awry

Richard Thaler was awarded the 2017 Nobel Prize in Economic Sciences for his work persuading economists to pay more attention to human behavior — and for governments to pay more attention to economics. His best-selling book, “Nudge,” was about helping people make better decisions.

A typical 401(k) plan menu typically offers dozens of fund choices, each with its own array of disclosures and fees. The idea of reviewing all these individual funds in detail to find the “right” investment mix can be overwhelming. Many people become paralyzed with this abundance of choice and stick with the default option: the target-date fund.

Thaler’s retirement plan nudges have undoubtedly improved the lot of many who, left to their own devices, would not have participated in their companies’ 401(k) plans at all or, if they participated, would not have invested in equities.

On the other hand, this same nudge toward target-date funds as the default and often as the only retirement plan selection has set the stage for a different crisis: too many retirees outlasting their money in longer retirement periods.

Sophisticated investors, either on their own or with the support of a knowledgeable financial adviser, should adopt a radically different asset allocation methodology that is much more heavily weighted toward equities.

BEHAVIORAL TAKEAWAY

Choice architecture is the design of different ways in which choices can be presented to consumers and considers the impact of that presentation on decision making. The number of choices, the description of attributes, and the presence of a default choice all make a difference. Before selecting the default choice, it’s critical to understand all the implications and long-term consequences of that choice.

Timothy Keating is the president of Keating Wealth Management, a financial planning and investment advisory firm. He has 34 years of Wall Street experience, previously serving as the CEO and founder of a publicly traded closed-end fund focused on pre-IPO investing.