Upcoming Event

Free Newsletter

Free Newsletter

In finance, even the winners can lose

James Osborne //February 5, 2014//

I love reading, talking and thinking about investing. It is a big part of why I am in this business. The financial markets are fascinating machines, part profit-seeking mechanical beast and part emotionally-driven human marketplace. It is important (and fun) for me to stay informed, so I try to do so regularly. (For some ideas of what I typically read, try here, here and here.) On a regular basis I read, scan, skim and digest and good amount of data, commentary, history and information. It’s fun and provides good fodder for conversation with other financial professionals, clients and other folk.

But not much of this information is truly actionable. Janet Yellen is the new Fed chair? Cool, let’s talk about it, but I’m not going to try to time the bond market all of a sudden. Everyone wants to talk about CAPE ratios, historical valuations, profit margins, and labor share of income? Fascinating stuff from an academic perspective, but I’m not going to assume this information/discussion is a new tool that will suddenly make market timing successful.

The fact of the matter is, you can get everything right about what you expect to happen with the global economy, profit margins, valuations, taxes, foreign policy, exchange rates, unemployment, real estate value, interest rates, Fed policy, fiscal policy and the weather and still get the investment side wrong. There are just too many ways that you can be wrong. You can be wrong about the timing of these events. You can be wrong about the magnitude of these events. You can be wrong about the interrelationships of these events. You can be wrong about how stock and bond markets react to these events. You can be wrong about investor sentiment.

In the last five years PIMCO has been a perfect example of this. Coming out of the recession in ’08-’09, PIMCO’s Bill Gross and (former co-CIO) Mohamed El-Erian proclaimed that the “New Normal” was upon us. Here’s an outtake from Gross’ September 2009 newsletter:

…New Normal, which is a period of time in which economies grow very slowly as opposed to growing like weeds, the way children do; in which profits are relatively static; in which the government plays a significant role in terms of deficits and reregulation and control of the economy; in which the consumer stops shopping until he drops and begins, as they do in Japan (to be a little ghoulish), starts saving to the grave.”

Now Gross and El-Erian are no fools. Gross runs one of the world’s largest bond portfolios and has built PIMCO into a giant. El-Erian is regarded by many as brilliant, formerly managed Harvard’s $35 billion endowment and served 15 years at the International Monetary Fund. These two guys are not slackers. Among the themes were the the ideas that risk assets (such as stocks) would underperform, foreign investments would outpace US as the US dollar would fall, corporate profits would stagnate and consumers would stop spending.

Now, Gross got many of the macro, big picture calls correct. GDP growth has been lower than traditional recovery levels since the recession. Consumers did deleverage, reducing their outstanding debts to the point that debt service is now a smaller part of their spending than it has been in 20 years. Central banks continue to intervene in the markets.

But how did his message work out as an investment thesis? Pretty terribly. Since late 2009 Treasury rates have fallen slightly, offering reasonable returns. But US stock markets have rallied, boosted by growing earnings from corporate America. The US Dollar is marginally lower since late ’09 but not enough to offset the fact that US stocks have handily outperformed their foreign counterparts.

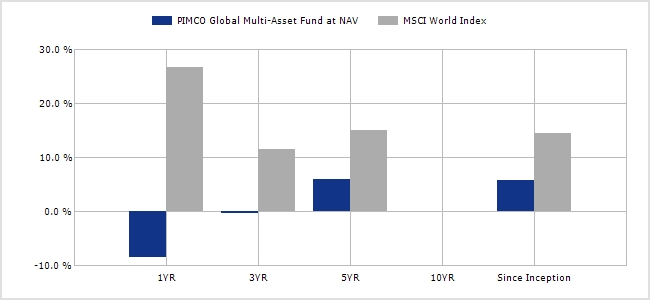

But the best way to review whether these calls are truly actionable or merely interesting is to review the performance of the strategies offered. PIMCO offers their “Global Multi-Asset Fund” which is based on (from PIMCO) “PIMCO’s full toolkit: our rigorously developed global macro outlook, our robust bottom-up security analysis and our research teams’ deep reservoir of specialized investment expertise.” So how did they do? Straight from PIMCO’s website, performance through 12/31/2013.

The fund underperformed a global stock market benchmark by nearly 35 percent last year. Over the trailing three and five years, it has not done much better, underperforming by over 10 percent annually over these periods. Even it it’s Lipper fund category (Global Flexible Portfolio), the fund is in the fifth quintile (bottom of the barrel) over one, three and five year periods.

In truth, it is not fair to just pick on PIMCO. Many well regarded firms offer similar strategies run by brilliant minds. These include Research Affliates’ Rob Arnott, Cambria’s Meb Faber and others. I’m not here to pick on these guys – they are MUCH smarter than I am. They are Ph.D.s and CFAs and have an understanding of economies and markets that makes me look like a kindergartner. But applying even the deepest understanding of the investment world to a real-life investment strategy can be difficult. Here’s how a few of the largest macro/tactical funds have fared. For comparison I included Vanguard’s Lifestrategy Moderate Growth portfolio, a relatively basic mix of 60 percent global stocks and 40 percent bonds.

Performance Through 12/31/14

1 Year

3 Years

5 Years

PIMCO Global Multi-Asset Fund Instl

-8.39%

-0.25%

5.99%

Eaton Vance Global Macro Absolute A

-0.55%

0.83%

3.47%

PIMCO All Asset All Authority Instl

-5.47%

4.64%

8.64%

Cambria Global Tactical ETF

1.80%

0.20%

N/A

Vanguard Lifestrategy Moderate Growth

15.04%

8.84%

11.94%

Depicted:

That giant red bar is the Vanguard fund putting these complex strategies to shame. So let’s keep bantering, tweeting, discussing, reading, and writing about the markets, economy and investment strategies. But let’s stop assuming that all of that discussion is going to do much for our investment results. It’s a whole lot of fun and a good mental exercise — and little else.